AI Infrastructure Boom: Bubble, Gold Rush, or the Next Industrial Revolution?

Something enormous is happening beneath the surface of the economy, and most people are only seeing the shiny front end of it. They see ChatGPT, Gemini, Claude, image generators, coding assistants, AI search tools, and companies rushing to put “AI-powered” on every product page. What they do not always see is the physical machine being built underneath all of it: data centers, chips, power lines, cooling systems, storage drives, networking gear, fiber optics, transformers, and grid capacity.

That hidden machine is the real AI infrastructure boom. It is not just a software trend. It is a capital-intensive industrial buildout involving some of the largest companies in the world. Microsoft, Amazon, Alphabet, Meta, Nvidia, utilities, semiconductor suppliers, storage companies, optical networking firms, and construction-heavy data center operators are all being pulled into the same gravitational field.

This is why the AI boom feels different from a normal tech cycle. In the smartphone era, the winners were the companies that owned the app stores, devices, operating systems, and social platforms. In the AI era, at least for now, the biggest winners may be the companies selling the “picks and shovels” required to run the whole system. The gold rush comparison is overused, but in this case it is useful: before anyone knows which AI apps will become dominant, everyone already knows that the AI economy needs chips, electricity, memory, storage, networking, and data centers.

The real question is whether this is the foundation of the next industrial revolution or the most expensive bubble since the dot-com era. The honest answer is uncomfortable: it could be both. The technology may be real, the spending may be necessary, and the long-term impact may be massive — while many investors still overpay for the wrong companies at the wrong time.

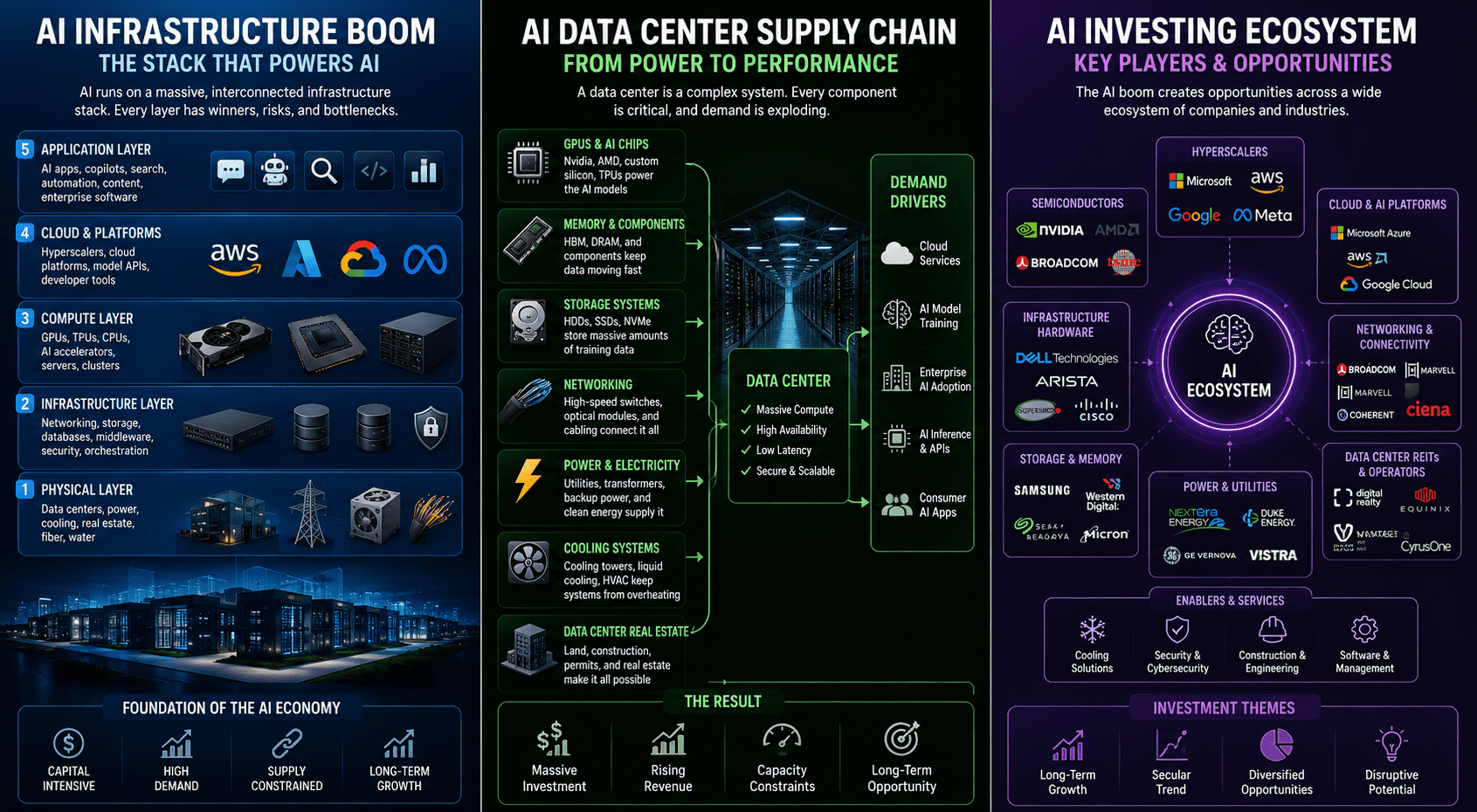

What Is the AI Infrastructure Boom?

The AI infrastructure boom is the rapid expansion of the physical and digital systems required to train, deploy, and operate artificial intelligence at scale. It includes the obvious pieces, like GPUs and data centers, but it also includes less glamorous parts of the stack: energy supply, backup power, cooling equipment, storage drives, optical transceivers, networking chips, construction permits, land, water, transformers, and specialized labor.

That matters because AI is not magic floating in the cloud. Every time a user asks a model to write code, generate an image, summarize a document, analyze a spreadsheet, or automate a business process, that request runs through real hardware somewhere. The “cloud” is just someone else’s building full of machines, plugged into someone else’s power grid.

Nvidia’s latest earnings show why investors are paying attention. The company reported record first-quarter fiscal 2027 revenue of $81.6 billion, up 85% from a year earlier, and record data center revenue of $75.2 billion, up 92% from a year earlier. Nvidia also said data center compute revenue reached $60.4 billion and data center networking revenue hit $14.8 billion under its previous reporting categories.

Those are not small numbers for a niche technology. They are industrial-scale numbers. Nvidia’s CEO Jensen Huang described the buildout of “AI factories” as one of the largest infrastructure expansions in history, and while CEOs naturally talk their book, the revenue growth suggests the demand is not imaginary.

Why This Boom Fascinates Investors

Investors are fascinated by the AI infrastructure boom because it gives them something concrete to invest in. Predicting which AI app will dominate five years from now is difficult. Predicting that AI systems will need more compute, power, memory, and storage is much easier.

This is the appeal of the picks-and-shovels strategy. Instead of betting on every miner in the gold rush, you bet on the companies selling shovels, denim, rail access, maps, and tools. In today’s version, that could mean semiconductors, cloud providers, networking companies, electrical equipment suppliers, cooling systems, storage manufacturers, and utilities connected to data center growth.

Microsoft is one of the clearest examples. In its fiscal 2026 third-quarter results, Microsoft said its AI business surpassed a $37 billion annual revenue run rate, up 123% year over year. It also reported Microsoft Cloud revenue of $54.5 billion, up 29%, and commercial remaining performance obligation of $627 billion.

Alphabet is another example. In its first-quarter 2026 earnings call, Alphabet said capital expenditures were $35.7 billion in the quarter, with the overwhelming majority going toward technical infrastructure to support AI opportunities. It also said about 60% of that technical infrastructure investment went into servers and 40% went into data centers and networking equipment.

Meta is spending heavily too. The company raised its 2026 capital expenditure guidance to a range of $125 billion to $145 billion, citing higher component pricing and additional data center costs for future capacity.

Amazon is also deep in the buildout. Business Insider reported that Amazon’s first-quarter 2026 capital expenditures totaled $43.2 billion and that Amazon had previously said it planned to spend $200 billion on capex this year, much of it focused on AI infrastructure.

The newsletters you provided framed this as roughly a $700 billion capital expenditure wave among the four largest hyperscalers, with Amazon, Alphabet, Microsoft, and Meta all pushing huge AI infrastructure budgets. The useful part of that claim is not the exact number. The useful part is the pattern: the biggest technology companies are not talking about AI casually. They are allocating real capital at enormous scale.

Why the Bulls Think This Is Real

The bull case starts with one simple argument: the demand is real because the customers are already there. AI is being embedded into cloud services, coding tools, customer support systems, search engines, advertising products, productivity software, cybersecurity tools, and enterprise workflows. Companies are not merely experimenting anymore; many are trying to rebuild their operations around AI.

The biggest cloud providers are also reporting supply constraints. In plain English, that means customers want more AI compute than the companies can currently provide. That is very different from a bubble where companies build infrastructure and then hope demand appears later.

Alphabet’s cloud results are a strong example. Google Cloud revenue was up 63% to $20 billion in the first quarter of 2026, and Alphabet said Google Cloud’s backlog nearly doubled sequentially to $462 billion. Alphabet connected that backlog growth to enterprise AI demand and TPU hardware sales.

That is a serious point in favor of the bulls. If AI demand is showing up in cloud backlog, data center contracts, chip purchases, and enterprise software adoption, then the infrastructure boom is not purely speculative. It may be aggressive, expensive, and risky, but it is being driven by actual usage.

The second bull argument is that AI infrastructure has bottlenecks. Advanced chips cannot be produced overnight. Data centers take time to build. Grid connections take planning. Power generation and transmission are slower-moving than software. Skilled labor, land, permitting, cooling capacity, memory supply, and optical networking all matter.

Bottlenecks create pricing power. If demand rises faster than supply, suppliers can charge more, protect margins, and sign long-term agreements. That is part of why companies like Nvidia have become so powerful. It is not just that they make popular chips. It is that the entire AI economy depends on hard-to-replace infrastructure.

The Power Grid Is Becoming the Real Constraint

The most underrated part of the AI infrastructure boom is electricity. Investors love talking about GPUs, but GPUs are useless without power. Data centers are not just computer buildings; they are huge electricity consumers that need stable, reliable, uninterrupted energy.

The International Energy Agency estimates that data centers consumed around 415 terawatt-hours of electricity in 2024, about 1.5% of global electricity consumption. In its base case, the IEA projects that global data center electricity consumption will double to around 945 terawatt-hours by 2030, growing around 15% per year between 2024 and 2030.

That is a huge shift because electricity systems move slower than software markets. A new AI app can launch in months. A major transmission project, power plant, or grid upgrade can take years. That mismatch is one reason power availability is becoming one of the key limits on AI growth.

Goldman Sachs Research recently projected that U.S. data center power demand could more than double from 31 gigawatts in 2025 to 66 gigawatts in 2027. Goldman also warned that only about 50% to 60% of scheduled data center capacity over the next one to two years is expected to come online on time because of delays and cancellations.

That matters for investors because it changes where the opportunity may be. If power becomes the bottleneck, then the AI infrastructure boom may benefit utilities, grid equipment suppliers, natural gas infrastructure, nuclear-related companies, backup power systems, energy storage providers, and electrical construction firms. It also means some data center projects may get delayed, repriced, or cancelled if they cannot secure enough electricity.

The newsletter content you provided picked up on this theme too, pointing to grid stress, PJM emergency pricing, Data Center Alley, and the idea that infrastructure cost models may need to be repriced if the grid limit is embedded rather than temporary.

Memory, Storage, and Networking: The Less Glamorous Winners

The AI infrastructure boom is bigger than Nvidia. That does not mean Nvidia is unimportant; Nvidia is arguably the central company in the current AI hardware cycle. But if investors only look at GPUs, they miss the rest of the machine.

AI models need memory to move data quickly. They need high-capacity storage to hold training data, customer data, logs, model weights, backups, and increasingly complex digital assets. They need networking systems to connect thousands of chips inside enormous data centers. They need optics, switches, routers, cables, and specialized components that most casual investors never think about.

This is where companies like Western Digital, Seagate, Applied Optoelectronics, Broadcom, Marvell, Coherent, Corning, Lumentum, and other infrastructure suppliers become interesting. Not all of them are guaranteed winners, and some may already be expensive, but the category itself matters.

The newsletter file noted that Western Digital’s fiscal Q3 2026 revenue was $3.34 billion, up 45.5% year over year, with 89% of revenue coming from cloud customers. It also said Western Digital sold 199 exabytes of nearline hard drives during the quarter, up 37% year over year, showing how AI and cloud demand are pulling storage into the investment story.

That is useful for readers because it expands the mental map. AI investing is not just “buy the most famous chip stock.” A smarter investor asks where the pressure is building across the full stack. If the cloud providers are spending hundreds of billions, then the money has to flow somewhere.

The danger is that once Wall Street finds a theme, it can overprice every stock connected to it. A good business can still be a bad investment if the valuation assumes perfection. That is where the AI infrastructure story starts to get risky.

The Bear Case: This Could Still Become a Bubble

The skeptical case does not say AI is fake. That is too simplistic. The stronger bear case says AI may be real, but the market may still overpay for the infrastructure required to build it.

This is an important distinction. The internet was real in 1999. That did not stop investors from losing fortunes in overvalued dot-com stocks. Railroads were real in the 1800s. That did not stop railroad bubbles and bankruptcies. Housing was real in 2006. That did not stop reckless financing from turning a real asset class into a disaster.

The same logic could apply to AI. Artificial intelligence may transform business, education, healthcare, manufacturing, entertainment, and software development. But if companies spend too much, depreciate hardware too slowly, build ahead of actual profitable demand, or assume endless growth, investors can still get hurt.

One concern is capital intensity. The AI boom requires enormous upfront spending. That can pressure free cash flow, especially when companies build infrastructure faster than revenue ramps. Amazon’s CFO discussion around capex captured this risk well: data centers can be long-lived assets, but when capital spending grows much faster than revenue, free cash flow can be challenged in the early years.

Another concern is obsolescence. AI hardware may improve so quickly that today’s expensive equipment becomes less competitive faster than expected. If a company depreciates AI chips over a long period but the chips become economically outdated sooner, reported profits may look better than the underlying economics.

There is also competition. Nvidia dominates the current AI accelerator market, but Alphabet has TPUs, Amazon has Trainium, AMD is competing, and other custom silicon efforts are underway. The newsletter content specifically flagged Google and Blackstone’s TPU commercialization as a possible challenge to Nvidia’s inference moat.

That does not mean Nvidia is doomed. It means investors should avoid lazy thinking. The best company today is not always the best-priced stock tomorrow, and the leader of one phase of a technology cycle does not automatically capture every phase that follows.

Why This Matters for Regular Investors

For regular investors, the AI infrastructure boom matters because it is now big enough to affect the entire market. This is not a tiny side trend tucked away in speculative tech stocks. AI-related spending is influencing mega-cap valuations, utility demand, electricity prices, semiconductor supply chains, bond market assumptions, and even job market expectations.

It also matters because many people are trying to improve their financial future while feeling squeezed by inflation, housing costs, job uncertainty, and unstable markets. When money feels tight, the temptation is to chase whatever trend looks like it can solve everything quickly. That is exactly when investors are most vulnerable to hype.

The right lesson is not “avoid AI.” That would be too defensive. The better lesson is “understand the layers.” AI may be one of the most important investment themes of the next decade, but not every AI stock is a good investment, not every infrastructure supplier will win, and not every expensive valuation will be justified.

A practical investor can break the theme into categories:

- Core platforms: Microsoft, Alphabet, Amazon, Meta, and other companies embedding AI into existing products.

- Hardware leaders: Nvidia, AMD, Broadcom, TSMC, and other semiconductor-linked names.

- Data center infrastructure: power systems, cooling, networking, optics, servers, and storage.

- Energy and utilities: companies tied to grid expansion, reliable electricity, and data center power demand.

- Risk controls: broad ETFs, cash, bonds, dividend stocks, and non-AI sectors to avoid overconcentration.

That last point matters. You do not need to bet your entire financial future on one stock or one trend. A person trying to build net worth should think in terms of survival first, compounding second, and upside third. The market rewards patience more consistently than panic.

How to Think About Investing in the AI Infrastructure Boom

The cleanest way to approach this theme is to separate the technology story from the investment decision. The technology story can be exciting while the investment decision still requires discipline.

Start by asking whether a company is selling into real demand or just borrowing the AI narrative. A company with signed cloud contracts, rising backlog, durable margins, and clear customer demand is different from a company that merely added “AI” to its investor presentation.

Next, ask where the company sits in the stack. Is it a must-have supplier, a replaceable vendor, a speculative startup, a utility with regulated returns, or a software company trying to prove monetization? The closer a company is to a bottleneck, the more pricing power it may have. The farther it is from real demand, the more careful investors need to be.

Then look at valuation. This is where people get into trouble. A strong company trading at a fair price can be a long-term wealth builder. A strong company trading at an absurd price can become dead money for years. A weak company trading at a hype valuation can be a disaster.

Also pay attention to debt and free cash flow. Infrastructure booms often require heavy borrowing and huge upfront spending. That can work beautifully when demand keeps rising, but it becomes painful when rates rise, projects delay, or customers pull back.

Finally, diversify. This is not exciting advice, but it is how people stay in the game. If AI keeps booming, you want exposure. If AI stocks correct sharply, you want enough balance that you are not forced to sell at the worst time.

The Job Market Angle: Infrastructure Creates Work, But Not Equally

The AI infrastructure boom also has a job market angle, and it is worth watching closely. AI may reduce demand for some types of repetitive digital work, but it also increases demand for infrastructure builders, technicians, electricians, data center operators, network engineers, cybersecurity workers, chip designers, cooling specialists, energy planners, and skilled trades.

That is a key point for readers who are worried about the future. The AI economy will not only be built by PhDs writing model architectures. It will also be built by people who install fiber, maintain servers, secure networks, wire buildings, inspect power systems, manage logistics, and troubleshoot the physical infrastructure behind the cloud.

This is especially relevant in places like Canada, where the job market can feel uncertain and where people are trying to figure out which skills still matter. AI may change office work faster than hands-on infrastructure work. That does not mean trades and technical jobs are immune, but it does suggest that people with hybrid skills — practical technical ability plus AI literacy — may be in a stronger position.

For someone trying to elevate their net worth, that matters. Investing is one side of the equation. Earning power is the other. The AI infrastructure boom may create opportunities not only in portfolios, but also in careers, contracting, consulting, cybersecurity, data center services, electrical work, energy systems, and niche content businesses that explain these changes to regular people.

What Could Go Wrong?

The biggest risk is that companies overbuild. If everyone assumes AI demand will rise forever, too much capital may chase the same opportunity. That can lead to excess capacity, falling prices, weaker margins, and disappointed investors.

The second risk is that AI monetization disappoints. Companies are spending enormous amounts on AI infrastructure because they believe the revenue will follow. If customers use AI tools heavily but do not pay enough to justify the infrastructure cost, the economics could get uncomfortable.

The third risk is grid delay. If data centers cannot secure electricity, projects may slip. If power prices rise too much, political pushback may increase. If utilities prioritize data centers while households face rising bills, regulators may get involved.

The fourth risk is competition and technological change. Custom chips, more efficient models, better inference methods, and new architectures could shift value away from today’s winners. That does not destroy the AI boom, but it can change who profits from it.

The fifth risk is investor behavior. People often buy the best story after the easy money has already been made. They chase headlines, ignore valuation, and assume a great theme guarantees a great return. It does not.

Final Verdict: Bubble, Gold Rush, or Industrial Revolution?

The AI infrastructure boom is probably not pure hype. The spending is real, the revenue growth is real, and the infrastructure needs are real. Nvidia’s data center numbers, Microsoft’s AI revenue run rate, Alphabet’s cloud backlog, Meta’s capex guidance, Amazon’s infrastructure spending, and global electricity demand forecasts all point to something much larger than a passing software fad.

But that does not mean every AI infrastructure investment is safe. The better way to think about it is this: the industrial revolution part may be real, while the bubble risk may show up in individual stocks, inflated valuations, weak companies, rushed projects, and investors who forget that price still matters.

For readers trying to build wealth, the best move is not to ignore AI and not to blindly chase it. The best move is to understand the stack, identify the bottlenecks, respect valuation, and avoid putting your entire future on one trade. AI infrastructure may become one of the defining investment themes of the decade, but the winners will not be evenly distributed.

The people who do best will probably be the ones who stay curious without getting reckless. They will study the real-world infrastructure, watch where capital is flowing, and build exposure carefully instead of gambling emotionally. That is how you turn a major trend into a serious wealth-building opportunity instead of another painful lesson.

Relevant External Links

NVIDIA First Quarter Fiscal 2027 Results

IEA Energy and AI: Data Centre Electricity Demand