Seller Financing to Buy a Business: How It Works in Canada and the U.S.

A lot of entrepreneurship advice makes buying a small business sound almost effortless: find a retiring owner, convince them to finance the sale, improve the website, modernize the marketing, and turn an “ugly” business into a money machine. There is a real business-acquisition strategy underneath that idea, especially in industries such as roofing, HVAC, plumbing, landscaping, restoration, trucking, fabrication, and commercial cleaning. These businesses may not look glamorous online, but many have long customer histories, local reputations, equipment, trained employees, and recurring demand.

The missing piece in most short-form videos is that buying a business is not simply a matter of finding a seller willing to wait for payment. Seller financing can make a deal more achievable, but it does not erase the need for cash flow, due diligence, lender approval, working capital, legal agreements, or operational skill. A buyer can inherit a functioning business with real customers, but they can also inherit underpriced jobs, weak staff retention, aging equipment, bad debts, customer concentration, or a reputation problem that no new website will fix.

Seller financing is worth understanding because it can bridge the gap between what a business costs and what a buyer can finance through their own cash, a bank, or a government-backed loan program. In Canada, it is commonly called vendor financing, a vendor note, or a vendor take-back (VTB). In the United States, it is generally called a seller note or seller financing. In both cases, the seller is effectively becoming one of the buyer’s lenders.

Seller Financing at a Glance

Seller financing is not a government grant, a loophole, or a way to buy a business without risk. It is a negotiated private financing arrangement between the buyer and seller.

Here is the basic idea:

- The buyer pays part of the purchase price at closing.

- A bank, credit union, BDC, SBA lender, or other lender may finance another portion.

- The seller agrees to leave part of the purchase price in the business as a loan.

- The buyer repays that seller-financed balance over time, normally with interest.

- The seller may have to wait behind the senior lender for repayment if the deal requires subordination.

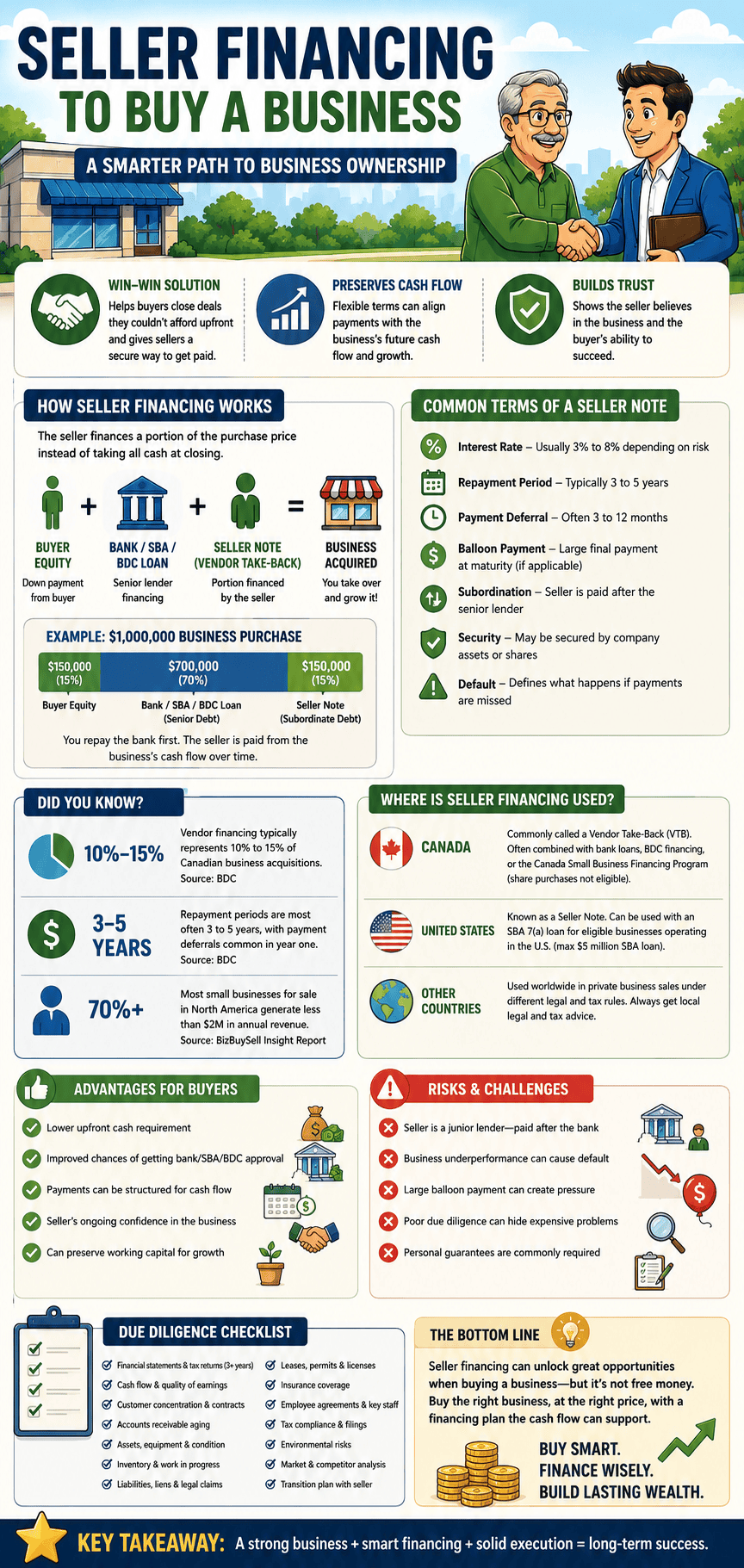

BDC describes vendor financing as a form of acquisition debt where part of the purchase price remains owed to the vendor. BDC also notes that vendor financing commonly represents roughly 10% to 15% of a transaction, although the actual amount depends entirely on the business, financing package, and negotiation.

The central lesson is simple: seller financing can improve a financing package, but it should never be treated as proof that the business is worth buying.

What Is Seller Financing When Buying a Business?

Seller financing happens when the person selling a business accepts a portion of the purchase price later rather than receiving every dollar on closing day. The unpaid balance becomes a debt owed by the buyer to the former owner. That debt is usually documented through a promissory note and included in the purchase agreement, financing documents, security documents, and other legal paperwork.

For example, imagine a small HVAC company is being sold for CAD $1 million. The buyer may contribute CAD $150,000 of their own money, obtain CAD $700,000 from a senior lender, and ask the seller to finance the remaining CAD $150,000. The seller receives CAD $850,000 at closing and holds a note for the remaining CAD $150,000. The buyer then repays the seller over an agreed period, perhaps through monthly payments, annual payments, interest-only payments at first, or another negotiated structure.

That example is only a financing illustration. It does not mean a lender will finance 70% of every deal or that a seller will automatically accept 15% as a vendor note. The price, debt terms, buyer contribution, collateral, business cash flow, and lender requirements all change from one acquisition to another.

In many transactions, seller financing is considered junior debt. That means the bank or primary lender is ahead of the seller in repayment priority. If the business struggles, the senior lender may need to be paid before the former owner receives payments. BDC notes that vendor financing is usually subordinate to bank loans and other senior financing, which is why sellers need to understand the risk before agreeing to it.

Why Would a Seller Finance the Buyer?

At first glance, seller financing seems strange. A retiring business owner has spent decades building a company, so why would they accept part of the sale price later instead of demanding all cash immediately?

The answer is that seller financing can help make a deal possible. A strong business may have substantial goodwill, customer relationships, reputation, trained staff, service contracts, and recurring revenue that a lender does not fully treat as collateral. A bank may be comfortable financing trucks, equipment, inventory, or a building, but more cautious about financing a company’s full asking price. A seller note can fill part of that valuation gap.

Seller financing can also show confidence. When a seller agrees to leave money in the business, they are signalling that they expect the company to remain viable after the transition. That does not guarantee the deal is good, but it can be more reassuring than a seller insisting on every dollar immediately while refusing to stand behind the company’s future performance.

Some sellers also want a smoother exit. They may be retiring, moving, dealing with health issues, or lacking a family successor. They may prefer a buyer who will keep the staff employed, preserve the company name, continue serving longtime customers, and protect the seller’s legacy. A vendor note can make that buyer’s offer more competitive than an all-cash offer from someone who plans to cut staff, merge the company, or strip assets.

Seller Financing Is Not the Same as an Earn-Out

Seller financing and earn-outs are often mentioned together, but they are not the same thing.

A seller note is a fixed debt obligation. The buyer owes a stated amount to the seller, usually with interest and a repayment schedule. The company may perform well or poorly, but the debt remains unless the agreement says otherwise.

An earn-out is contingent consideration. The seller receives additional money only if the business reaches agreed performance targets after closing. Those targets may involve revenue, EBITDA, gross profit, customer retention, contract renewals, or another measurable metric.

A seller note can be useful when the parties agree on the purchase price but need flexible financing. An earn-out is more useful when the buyer and seller disagree about future performance. For example, a seller may claim that a roofing company can grow rapidly once a new territory opens, while the buyer may believe that forecast is too optimistic. Rather than overpaying upfront, the buyer may agree to pay more later only if the forecast actually comes true.

Both structures require careful legal drafting. Earn-outs can create disputes because the seller may accuse the buyer of changing prices, reducing marketing, moving customers, delaying jobs, or running the business in a way that makes targets harder to hit. A seller note is simpler in concept, but it still needs clear rules for repayment, default, security, and lender priority.

Where Seller Financing Works: Canada, the U.S., and Beyond

Seller financing is not something a country “offers” in the same way it offers a grant or government loan program. It is a private business-sale structure. It can be used in many countries when the buyer and seller can legally agree to a deferred-payment arrangement and document it properly.

For Canadian buyers, the most common language is vendor financing, vendor note, or vendor take-back. A Canadian acquisition may combine personal cash, conventional bank financing, BDC financing, a Canada Small Business Financing Program loan, and a vendor note. The exact mix depends on whether the buyer is acquiring assets, shares, real estate, equipment, goodwill, or a combination of those items.

The Canada Small Business Financing Program can help lenders provide financing by sharing risk with them. For business acquisitions, the program says the purchase of eligible assets of an existing business may qualify, but financing is tied to the lower of the purchase cost or the appraised value of eligible assets. Share purchases are not eligible under the program, which matters because many business purchases are structured as share transactions rather than asset purchases.

BDC also offers business-purchase and transfer financing, including financing for existing businesses, goodwill, client lists, intellectual property, and refinancing vendor take-backs. That makes BDC particularly relevant when the acquisition price includes significant intangible value that does not fit neatly into an equipment-backed bank loan.

For American buyers, the most commonly discussed government-backed acquisition product is the SBA 7(a) loan. The SBA does not lend directly to borrowers; instead, it guarantees qualifying loans made by participating lenders. The 7(a) program can be used for complete or partial changes of ownership, and its maximum loan amount is generally US $5 million. The business must operate in the United States, so an SBA loan is not a financing option for buying a Canadian business.

How Seller Financing Fits Into a Business Acquisition

Most business purchases use a capital stack, meaning several sources of money are combined to fund the deal. A typical capital stack may include buyer equity, senior debt, seller financing, working-capital facilities, and sometimes outside investors.

The senior lender normally wants to know whether the business can comfortably service its debt. That means looking beyond headline revenue and focusing on actual cash flow. A company can generate CAD $2 million in revenue while still being a poor acquisition if it has low margins, expensive crews, slow-paying customers, warranty claims, excessive owner perks, or equipment that needs immediate replacement.

The seller note can help bridge a gap, but it cannot make weak cash flow strong. If the business cannot afford the primary loan, seller note, payroll, tax obligations, repairs, marketing, and owner compensation, adding more debt simply creates a delayed problem. Buyers who focus only on “how can I get approved?” often ignore the more important question: “Can this business safely pay everyone after I take over?”

A realistic acquisition model should include monthly projections for revenue, gross margin, payroll, rent, insurance, vehicle costs, fuel, materials, debt payments, tax obligations, required equipment replacement, and working-capital needs. It should also test a bad scenario, not only the seller’s best year.

Common Terms in a Seller-Financed Deal

The seller note needs more detail than “I will pay you back over time.” Before signing, both sides should understand exactly what is being financed and what happens if the business performs poorly.

Important terms often include:

- Principal amount: The unpaid portion of the purchase price owed to the seller.

- Interest rate: The cost of borrowing the seller-financed amount.

- Amortization period: The schedule used to calculate payments.

- Maturity date: The date the remaining balance must be fully repaid.

- Balloon payment: A large final payment due at maturity after smaller payments during the term.

- Payment deferral: A period where payments are delayed or reduced to protect early cash flow.

- Subordination agreement: A document confirming that the senior lender has repayment priority over the seller.

- Security: Assets or shares pledged to support repayment of the seller note.

- Default terms: What happens if the buyer misses payments, breaches a covenant, or sells assets without approval.

- Transition obligations: The seller’s role after closing, including training, introductions, customer handoffs, and staff transition.

BDC notes that vendor-financing repayment periods are often three to five years and that payments may sometimes be deferred during the first year. Those are common deal patterns, not universal rules.

A buyer should not casually agree to a short seller note with a major balloon payment. If the note comes due before the business has built enough cash or qualified for refinancing, the buyer may face a serious liquidity problem. A deal that looks manageable on monthly payments can become dangerous when a large final balance is due.

Why “Ugly Businesses” Can Be Attractive

The phrase “ugly business” usually does not mean a bad business. It means a business that is operationally valuable but not trendy, exciting, or polished.

A residential roofing company, HVAC contractor, septic-service business, commercial cleaning company, equipment-rental operation, or niche industrial supplier may have boring branding, an outdated website, paper invoices, slow lead response, and weak social media. Yet it may also have decades of local customer trust, repeat work, referral business, experienced crews, and a useful place in the local economy.

Modernizing these businesses can create real value. Better online booking, quote follow-up, customer relationship management software, call tracking, local SEO, review systems, route planning, automated reminders, digital invoicing, and faster response times can improve the customer experience. But modernization only works when the underlying operations are healthy.

A new website cannot repair a company that consistently underbids jobs. Social media cannot solve poor workmanship. Automation cannot compensate for a business that loses its best technician, relies on one major customer, or has liabilities hidden in messy books. The goal is not to buy a failing company and hope technology saves it; the goal is to buy a solid company with operational upside.

Due Diligence Matters More Than the Financing Pitch

Seller financing should make a buyer more careful, not less careful. The seller may be willing to finance part of the deal because they believe in the business, but they may also be doing it because the asking price is difficult to support through traditional financing.

Before agreeing to a purchase, a buyer should investigate the business from multiple angles:

- Review several years of financial statements, tax filings, bank records, and management reports.

- Recalculate earnings after removing unusual expenses, owner perks, one-time income, and questionable adjustments.

- Examine customer concentration, repeat revenue, contracts, backlog, warranty exposure, and customer churn.

- Review accounts receivable aging, accounts payable, inventory quality, deferred revenue, deposits, and unpaid tax obligations.

- Inspect equipment, vehicles, leases, licenses, permits, insurance coverage, employment agreements, and maintenance records.

- Search for lawsuits, liens, security interests, environmental risks, regulatory issues, and unresolved customer disputes.

- Speak with a lawyer, accountant, lender, and industry expert before closing.

For smaller owner-operated companies, a buyer may review seller’s discretionary earnings (SDE), which measures the cash flow available to one owner after adding back certain owner-specific expenses. Larger acquisitions often focus more heavily on EBITDA, meaning earnings before interest, taxes, depreciation, and amortization. Neither measure should be accepted blindly. The buyer must understand what has actually been added back and whether those expenses will truly disappear after the seller leaves.

Asset Purchase vs. Share Purchase

One of the biggest decisions in a business acquisition is whether to buy the company’s assets or its shares.

In an asset purchase, the buyer purchases selected assets such as equipment, inventory, customer lists, intellectual property, contracts, and goodwill. This can give the buyer more control over what is included and excluded, although contracts, permits, employees, and lease arrangements may need separate attention.

In a share purchase, the buyer acquires ownership of the corporation itself. This can make the transition smoother for certain contracts, licences, banking relationships, and assets, but it can also expose the buyer to more of the company’s historic liabilities. The right structure depends on the business, tax consequences, seller preferences, financing requirements, and legal risks.

This is not a decision to make from a YouTube short or a template purchase agreement. A lawyer and accountant should review the structure before an offer becomes binding. The purchase price may be identical on paper, but the risk, taxes, depreciation opportunities, liabilities, and financing implications can differ dramatically.

A Smarter Way to Approach a Seller-Financed Acquisition

A disciplined buyer should build the deal from the business outward, not from the financing backward. Start with a business that has durable demand, understandable operations, defensible margins, reasonable customer concentration, and a realistic handover plan.

Then build the financing package around the actual economics. If the company only works when everything goes perfectly, it is not a strong acquisition. You need room for slow seasons, customer losses, equipment repairs, hiring mistakes, delayed receivables, and the fact that a new owner usually makes mistakes during the first year.

A practical acquisition process often looks like this:

- Define the type of business, geography, price range, and industry you understand.

- Review the company’s financial performance before discussing creative financing.

- Sign a confidentiality agreement and request detailed financial and operational information.

- Submit a letter of intent that outlines price, financing assumptions, due diligence, and transition expectations.

- Speak with lenders early to understand what portion of the deal they may support.

- Negotiate the seller note only after understanding senior-lender requirements.

- Close only after legal, accounting, operational, and financing reviews are complete.

The strongest seller-financed deal is not the one with the smallest down payment. It is the one that gives the buyer enough cash flow, working capital, operating flexibility, and transition support to survive the first few years of ownership.

Final Thoughts

Seller financing can be a powerful way to buy an established business without paying the entire purchase price upfront. For Canadian buyers, vendor take-backs can work alongside bank financing, BDC acquisition financing, and, in some cases, Canada Small Business Financing Program lending. For U.S. buyers, a seller note may also be part of an acquisition financed with an SBA 7(a) loan.

The opportunity is real, especially in stable service businesses run by owners who are ready to retire. But the winning strategy is not “find an old business and borrow everything.” It is finding a fundamentally healthy company, paying a defensible price, structuring debt that the cash flow can support, and improving the business without destroying what made customers trust it in the first place.

Seller financing should make a good deal easier to close. It should never be used to force a bad deal into existence.

Related External Links

- BDC: Vendor Financing for Mergers and Acquisitions — Explains how vendor take-backs work in Canadian business-acquisition transactions.

- U.S. Small Business Administration: 7(a) Loans — Covers SBA-backed 7(a) financing, including its use for business ownership changes.