SBA Loans Explained: 7(a), 504, Microloans, and Canadian Alternatives

Getting financing is one of the biggest dividing lines between having a business idea and actually owning or growing a business. A contractor may need trucks and equipment, a retailer may need inventory, a growing service company may need working capital, and an aspiring entrepreneur may want to buy an established business from a retiring owner. In the United States, many people begin that conversation with an SBA loan because the Small Business Administration helps lenders take on qualified small-business loans that might otherwise be difficult to approve.

The important word is helps. The SBA is not a magic source of cheap money, and an SBA-backed loan is not a guarantee that a borrower will be approved. A lender still has to believe the business can repay the debt, the borrower is credible, and the financing request has a sound business purpose. For readers in Canada, there is another important distinction: SBA loans are U.S. programs, so they are not a financing option for a business operating in Canada.

Quick Answer: What Is an SBA Loan?

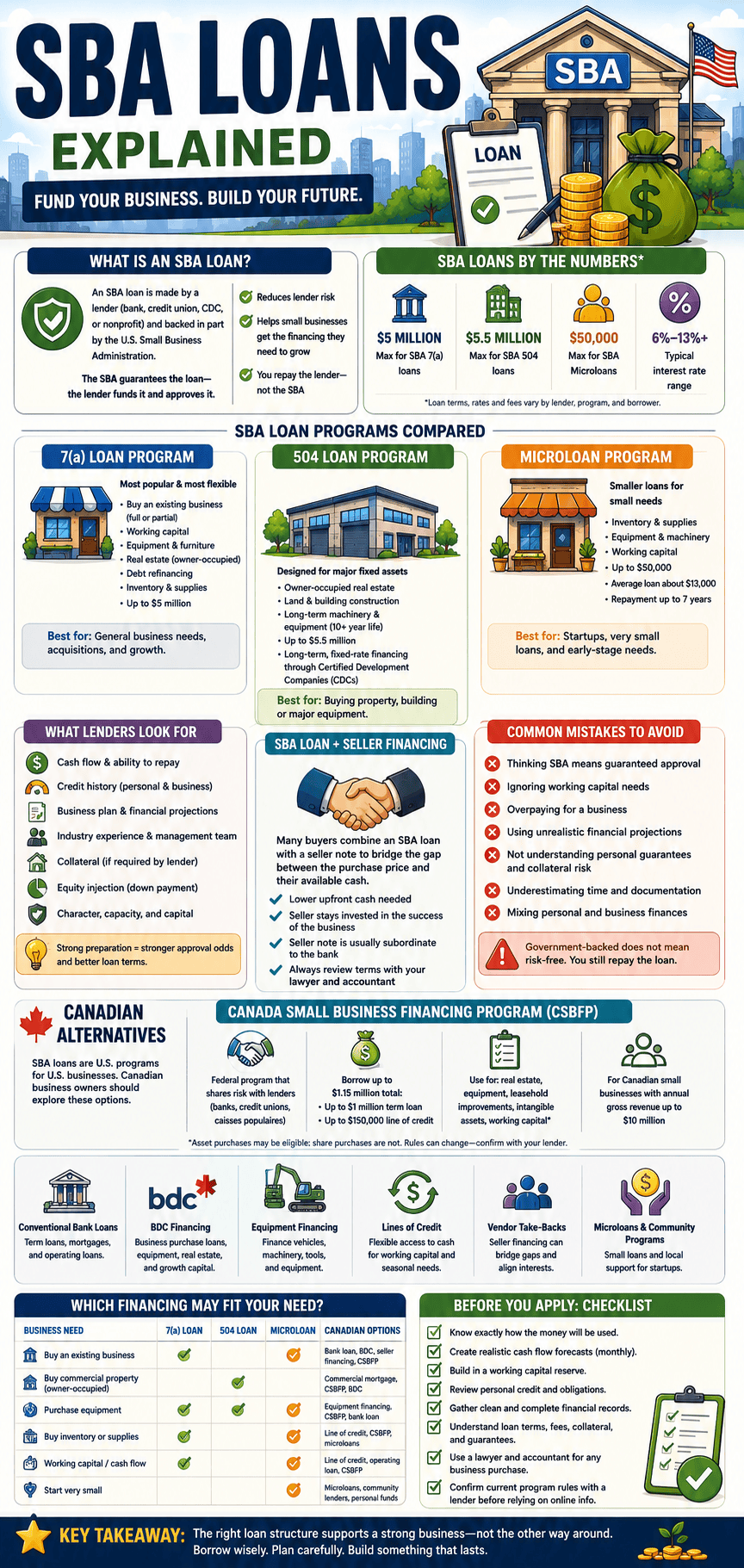

An SBA loan is a business loan made by a private lender and backed in part by the U.S. Small Business Administration. The SBA sets program rules and reduces some of the lender’s risk through a loan guarantee, but the borrower applies through a participating lender—not directly to the SBA in most normal business-financing situations. The lender approves the loan, sets its underwriting requirements, and collects the payments.

The three SBA programs most entrepreneurs hear about are:

- SBA 7(a) loans: Flexible financing for business purchases, working capital, equipment, real estate, refinancing, and ownership changes.

- SBA 504 loans: Long-term, fixed-rate financing for major fixed assets such as commercial property, construction, and long-life equipment.

- SBA Microloans: Smaller loans of up to US$50,000 for working capital, inventory, supplies, equipment, and similar needs.

The program can make financing more accessible, but it does not remove the fundamentals. You still need a reasonable business plan, credible cash-flow projections, financial records, sufficient working capital, and the ability to repay the debt if sales do not unfold exactly as planned.

How the SBA Loan System Actually Works

The most common misunderstanding is that the SBA directly hands entrepreneurs a business cheque. In reality, the SBA primarily works through banks, credit unions, specialized SBA lenders, Certified Development Companies, and nonprofit intermediaries. It sets guidelines and provides guarantees intended to reduce lender risk, while the lender remains responsible for reviewing the borrower and managing the loan. tinction matters because an SBA guarantee protects the lender, not the borrower from having to repay the loan. If the business fails, the borrower is still responsible for the debt and may have pledged business assets, personal assets, or signed personal guarantees. A government-backed loan should therefore be treated as a serious commercial obligation, not as low-risk startup money.

For the flagship 7(a) program, the SBA says eligible businesses generally must be for-profit, operating in the United States, small under SBA size standards, creditworthy, and able to show a reasonable ability to repay. The business must also fit within the program’s eligibility rules and generally be unable to obtain the desired credit on reasonable terms from other non-government sources. (a) Loans: The Flexible Business Financing Option

The SBA 7(a) program is the most broadly useful SBA loan program for ordinary business needs. It can be used for complete or partial ownership changes, working capital, equipment, furniture, supplies, real estate, debt refinancing, and multi-purpose business financing. The maximum 7(a) loan amount is currently US$5 million, although the amount an individual borrower can obtain depends on lender underwriting, repayment capacity, collateral, and program requirements. xibility is why 7(a) loans are often discussed when somebody wants to buy an established company. Imagine a buyer acquiring a plumbing company with a long operating history, experienced technicians, branded service vehicles, recurring maintenance work, and reliable cash flow. A 7(a) loan may be used to fund a portion of the purchase, while the buyer contributes equity and the seller agrees to finance another portion through a seller note.

This can create a more workable capital stack than expecting the buyer to provide the full purchase price in cash. The buyer’s money provides equity, the lender supplies senior debt, and the seller note can fill a negotiated gap. However, the lender will still examine whether the company’s cash flow can safely cover payroll, taxes, vehicle costs, insurance, materials, debt payments, and unexpected expenses after the ownership transition.

Most 7(a) term loans are repaid through monthly principal-and-interest payments funded by business cash flow. Rates and repayment terms vary by loan type, amount, use of funds, lender policies, and whether the rate is fixed or variable. Instead of chasing a headline interest rate, a borrower should model the total monthly obligation and test whether the business can still perform if revenue drops, labour costs rise, or receivables arrive late.

How 7(a) Loans Fit a Business Acquisition

A 7(a) loan can be particularly useful when the purchase price includes more than equipment and inventory. Many healthy small businesses are worth money because of their customer relationships, local reputation, contracts, systems, brand, and goodwill. Those intangible assets may not be as easy for a traditional lender to treat as collateral as a truck, building, or piece of machinery.

This is where the buyer needs discipline. A lender approving a loan does not mean the buyer has paid the right price. The buyer should still investigate customer concentration, recurring revenue, key employee retention, equipment condition, owner compensation, accounts receivable, warranty exposure, pending legal issues, and whether the seller’s claimed earnings will remain after the seller leaves.

The best acquisition is usually not the company with the flashiest pitch. It is the company with understandable operations, durable demand, clean financial reporting, realistic margins, and enough cash flow to survive an ordinary bad month. Financing should support a strong business; it should never be used to force a weak business into a deal it cannot carry.

SBA 504 Loans: Best for Property and Major Equipment

The SBA 504 loan program is built for major fixed assets rather than day-to-day operating needs. It provides long-term, fixed-rate financing through Certified Development Companies, or CDCs, which are community-based nonprofit partners certified and regulated by the SBA. The program’s maximum loan amount is currently US$5.5 million. an may be suitable for a growing manufacturer buying a larger facility, a contractor purchasing an owner-occupied commercial building, or a company acquiring long-life machinery with at least 10 years of useful remaining life. It can also support the construction of new facilities and the improvement or modernization of land and existing facilities. eoff is that 504 financing is more specialized than 7(a) financing. It cannot be used for ordinary working capital, inventory, speculative real-estate investing, or most soft business costs. That means a company buying a building may need a 504 structure for the property while using a separate source of financing for inventory, payroll, operating reserves, or the business purchase itself.

For an entrepreneur buying an existing HVAC, roofing, plumbing, or fabrication company, a 504 loan may make sense when commercial real estate is part of the deal. It is not normally the tool for funding goodwill, paying the seller for the full operating business, or carrying the company through its seasonal slow period. Those needs may call for 7(a) financing, conventional lending, seller financing, or a separate working-capital facility.

SBA Microloans: Small Capital for Early-Stage Needs

SBA Microloans are much smaller than 7(a) or 504 loans, but that does not make them unimportant. The program provides loans of up to US$50,000 through nonprofit, community-based intermediary lenders. The SBA reports that the average microloan is about US$13,000, which makes the program more relevant for focused purchases than for buying an established company. oan can be useful for inventory, supplies, furniture, fixtures, machinery, equipment, or working capital. A new mobile detailing business might use one for equipment and initial operating cash, while a small retail business could use one for inventory and fixtures. The funds cannot be used to repay existing debt or purchase real estate. n terms are set by each intermediary lender, and their credit requirements can vary. The SBA says intermediaries generally require some collateral and a personal guarantee from the business owner. The maximum repayment term is seven years, and the SBA says microloan interest rates generally range from 8% to 13%, depending on the intermediary. oan Programs at a Glance

| Program | Best For | Maximum Amount | Major Limits |

|---|---|---|---|

| SBA 7(a) | Buying a business, working capital, equipment, real estate, refinancing | US$5 million | Must meet SBA eligibility and lender underwriting requirements |

| SBA 504 | Owner-occupied property, construction, long-life machinery and equipment | US$5.5 million | Not for working capital, inventory, or speculative rental real estate |

| SBA Microloan | Small equipment purchases, inventory, supplies, and startup working capital | US$50,000 | Cannot be used for real estate or repaying existing debt |

The table is a starting point, not a substitute for lender guidance. A borrower may have a project that touches more than one category, such as buying a business that includes a building, operating equipment, inventory, and working capital. In that situation, the financing structure may involve multiple lenders or loan products.

What Lenders Look for Before Approving Financing

Lenders do not only assess the idea. They assess the borrower’s ability to operate and repay. A lender will want to understand what the money is for, how the business earns revenue, whether the borrower has relevant management or industry experience, and whether the projected cash flow can cover debt payments with a reasonable cushion.

For acquisitions, lenders will look closely at the target company’s historical financial results. A seller may present strong adjusted earnings, but the buyer and lender need to determine whether those adjustments are legitimate. Adding back the seller’s personal vehicle, travel, or one-time expenses may be reasonable; pretending that essential employee wages or recurring repairs will disappear is not.

A serious loan package often includes:

- Business and personal tax returns

- Personal financial statements and credit information

- Business financial statements and bank records

- Profit-and-loss statements and balance sheets

- Cash-flow forecasts and debt-payment projections

- Purchase agreement or letter of intent for an acquisition

- Equipment lists, leases, contracts, and customer information

- Details about seller financing, investor funds, or buyer equity

- A clear explanation of how the business will operate after closing

One term worth understanding is debt service coverage. This refers to how comfortably business cash flow can cover required loan payments. Lenders may calculate it differently, but the concept is straightforward: a business should produce more cash than it needs merely to make the debt payment. A deal that only works in the seller’s most optimistic forecast is too fragile.

Combining an SBA Loan With Seller Financing

Seller financing is one of the most practical ways to bridge a gap in a business acquisition. The seller agrees to leave part of the purchase price outstanding as a note instead of receiving every dollar on closing. The buyer then repays the seller over time, usually with interest and under negotiated terms.

In a U.S. acquisition, a seller note may work alongside an SBA 7(a) loan if the lender accepts the structure. The senior lender may require the seller note to be subordinate, meaning the bank has priority for repayment and collateral claims. That reduces the seller’s protection, which is why a seller willing to finance part of the deal may be showing confidence in the business—or may be helping make a high asking price financeable.

The smart buyer treats seller financing as one tool, not proof that the deal is safe. A seller note can preserve buyer cash and align the former owner with the company’s continued success. It can also add another monthly obligation, create pressure from a balloon payment, and increase the damage if the business underperforms after closing.

Common SBA Loan Mistakes to Avoid

The biggest mistake is treating approval as the finish line. Approval only means a lender believes the deal meets its lending standards; it does not guarantee that the business will be easy to operate or that the buyer will enjoy owning it.

Another mistake is borrowing for the purchase price while ignoring working capital. A new owner may take over a profitable business and still run into trouble because payroll arrives before customer invoices are paid, a truck needs replacement, material costs increase, or the seller’s best salesperson leaves. The cash needed to operate after closing is just as important as the cash needed to close.

Borrowers also need to be realistic about personal exposure. SBA-backed financing can involve collateral requirements and personal guarantees, depending on the program, ownership structure, lender, and loan terms. Do not sign documents based on a verbal summary from a broker or seller; read the commitment letter and loan documents carefully, and use a lawyer and accountant when the transaction is material.

Finally, avoid the “no-money-down business acquisition” mindset. Every deal has an equity requirement somewhere, whether it comes from the buyer, investors, retained cash, seller financing, or another source. The real goal is not to put in the least money possible. It is to build a financing structure that lets the business survive and grow without turning every slow month into an emergency.

Can Canadians Get SBA Loans?

An operating business in Canada is not eligible for an SBA 7(a) or 504 loan simply because the owner is Canadian or the business resembles an American small business. SBA 7(a) eligibility requires the business to operate in the United States, while 504 financing is for qualifying for-profit companies operating in the United States or its possessions. an entrepreneur considering the purchase of a U.S. business should speak directly with an SBA lender, cross-border lawyer, accountant, and immigration professional before assuming eligibility. Ownership, residency, business location, tax treatment, lender policy, and U.S. operating structure can all matter. The safe rule is simple: do not build a cross-border acquisition plan around an SBA loan until a qualified lender confirms that the proposed borrower and business structure fit current rules.

For Canadian business owners or buyers, the closest broad federal comparison is the Canada Small Business Financing Program, or CSBFP. Like the SBA model, it is not direct government lending. The federal government shares risk with participating financial institutions, but banks, credit unions, caisses populaires, and other lenders make the actual credit decision. P can support eligible small businesses in Canada with annual gross revenues of up to CAD $10 million. Current program information says borrowers may access up to CAD $1.15 million total: up to CAD $1 million in term loans and up to CAD $150,000 in lines of credit. Eligible financing can include commercial real property, equipment, leasehold improvements, intangible assets, and working capital, but an acquisition must be structured carefully because the purchase of eligible assets may qualify while share purchases are not eligible. ian Alternatives to Consider

Canadian entrepreneurs do not need an SBA program to finance a business, but they do need to understand which product fits the deal. A conventional bank term loan may work for equipment or a profitable established business. Equipment financing can suit vehicles, machinery, and tools. A line of credit may be better for seasonal cash flow, inventory, payroll timing, and short-term operating needs.

For acquisitions, BDC financing can also be relevant. BDC’s business-purchase financing describes support for buying an existing business, refinancing vendor take-backs, and financing intangible assets such as goodwill and client lists. matter because the value of a good business is often much larger than its visible equipment.

A quick Canadian financing comparison looks like this:

| Business Need | Financing to Explore |

| Buy a profitable existing business | Conventional acquisition loan, BDC financing, vendor take-back |

| Buy equipment, vehicles, or machinery | Equipment financing, bank term loan, CSBFP term loan |

| Purchase or renovate commercial property | Commercial mortgage, CSBFP, BDC, conventional bank financing |

| Fund seasonal payroll or inventory | Line of credit, operating loan, CSBFP line of credit |

| Cover part of a business purchase price | Buyer equity, lender financing, seller financing, outside investors |

| Start very small with limited capital | Microloans, community lending programs, equipment financing, personal savings |

Before You Apply: A Practical Checklist

Before approaching a lender, prepare the business case as though you are trying to convince a cautious partner to put their own money into it. That mindset produces better documents and forces you to find weaknesses early.

- Clarify exactly what the money will buy and why it will create value.

- Build a monthly cash-flow forecast, not just an annual revenue estimate.

- Include debt payments, taxes, payroll, insurance, rent, repairs, and owner compensation.

- Keep a working-capital reserve in the plan.

- Review your personal credit and existing obligations before applying.

- Gather clean financial records for any business you intend to buy.

- Verify whether a seller note, investor funds, or buyer equity must be subordinated or documented in a specific way.

- Have a lawyer and accountant review an acquisition before you sign binding documents.

- Confirm current program rules directly with an SBA lender or Canadian financial institution before relying on online guidance.

Final Thoughts

SBA loans can be powerful tools for American entrepreneurs because they make it possible to finance business growth, ownership changes, fixed assets, equipment, and operating needs through lender-backed programs. The 7(a) program is the flexible workhorse, the 504 program is designed for major fixed assets, and Microloans can help businesses that need a smaller amount of targeted capital.

The bigger lesson is that the right financing follows the business model. A 7(a) loan may be excellent for acquiring a service company with healthy cash flow, while a 504 loan may fit the purchase of a building or heavy equipment. A Canadian buyer may need a different combination of conventional lending, BDC financing, the CSBFP, equipment financing, and vendor take-back debt.

Do not choose a loan because it sounds prestigious, government-backed, or easy to market in a social-media clip. Choose the structure that gives the business the best chance to operate through normal setbacks, repay its obligations, and build durable value over time.

Related External Links

- U.S. Small Business Administration: SBA Loan Programs — Official overview of SBA 7(a), 504, Microloan, lender-match, and other business-loan options.

- Government of Canada: Canada Small Business Financing Program FAQ — Current eligibility, maximum financing amounts, eligible costs, and application information for Canadian businesses.