The Consumer Squeeze: What Home Depot, Walmart, Target, and McDonald’s Are Telling Investors

A recession does not always arrive with a giant warning sign. Sometimes it shows up quietly in smaller shopping carts, fewer gallons at the gas pump, delayed renovation projects, cheaper restaurant orders, and consumers suddenly caring a lot more about coupons, delivery fees, and value menus. That is why retail earnings matter so much right now.

For regular investors, the consumer squeeze is one of the most important signals in the market. It tells you whether households are still confident enough to spend, whether companies still have pricing power, and whether the economy is bending or breaking. You do not need to be a Wall Street analyst to understand this. You just need to watch where people are still spending, where they are pulling back, and which companies are gaining traffic when everyone feels broke.

That is the story behind Home Depot, Walmart, Target, and McDonald’s. These companies are not just stores and restaurants. They are economic sensors. Home Depot tells you whether homeowners are still confident. Target tells you how the middle-class discretionary shopper is behaving. Walmart tells you whether consumers are trading down for value. McDonald’s tells you whether even cheap convenience is still affordable.

The scary part is that consumers are not all sending the same signal. Some companies are still growing. Some are beating expectations. Some are guiding cautiously. Some are attracting higher-income shoppers who are looking for bargains. That means the economy may not be collapsing, but it is clearly becoming more selective. For investors, that selectivity is where both danger and opportunity live.

What Is the Consumer Squeeze?

The consumer squeeze is what happens when household costs rise faster than household comfort. People may still have jobs, still shop, still eat out, and still spend money, but they become more careful. They delay big purchases, switch brands, buy smaller quantities, trade down to cheaper retailers, and cut back on anything that feels optional.

This matters because consumer spending is a huge part of the economy. When households feel strong, businesses feel it. Retailers sell more, restaurants see more traffic, banks collect more fees, travel companies get bookings, and small businesses get customers. When households feel stretched, the pressure spreads outward.

The squeeze does not hit everyone equally. Higher-income households may still travel, renovate, and invest. Middle-income households may become more selective. Lower-income households may feel pressure immediately from food, rent, gasoline, debt payments, and insurance costs. This is why people talk about a “K-shaped” economy: some households move higher while others fall behind.

That is also why investors should not ask only, “Are sales up?” They should ask better questions. Are sales up because people are buying more, or because prices are higher? Are customers buying premium products, or trading down? Is traffic rising, or is the average basket shrinking? Are margins improving, or are companies absorbing costs to keep shoppers loyal?

Why Home Depot Matters: The Protected Consumer Test

Home Depot is a powerful consumer signal because its core customer is often a homeowner. That matters. Homeowners usually have more financial stability than renters. Many have home equity, retirement accounts, higher credit access, and more wealth tied to the stock market and housing market. If this group starts hesitating, investors should pay attention.

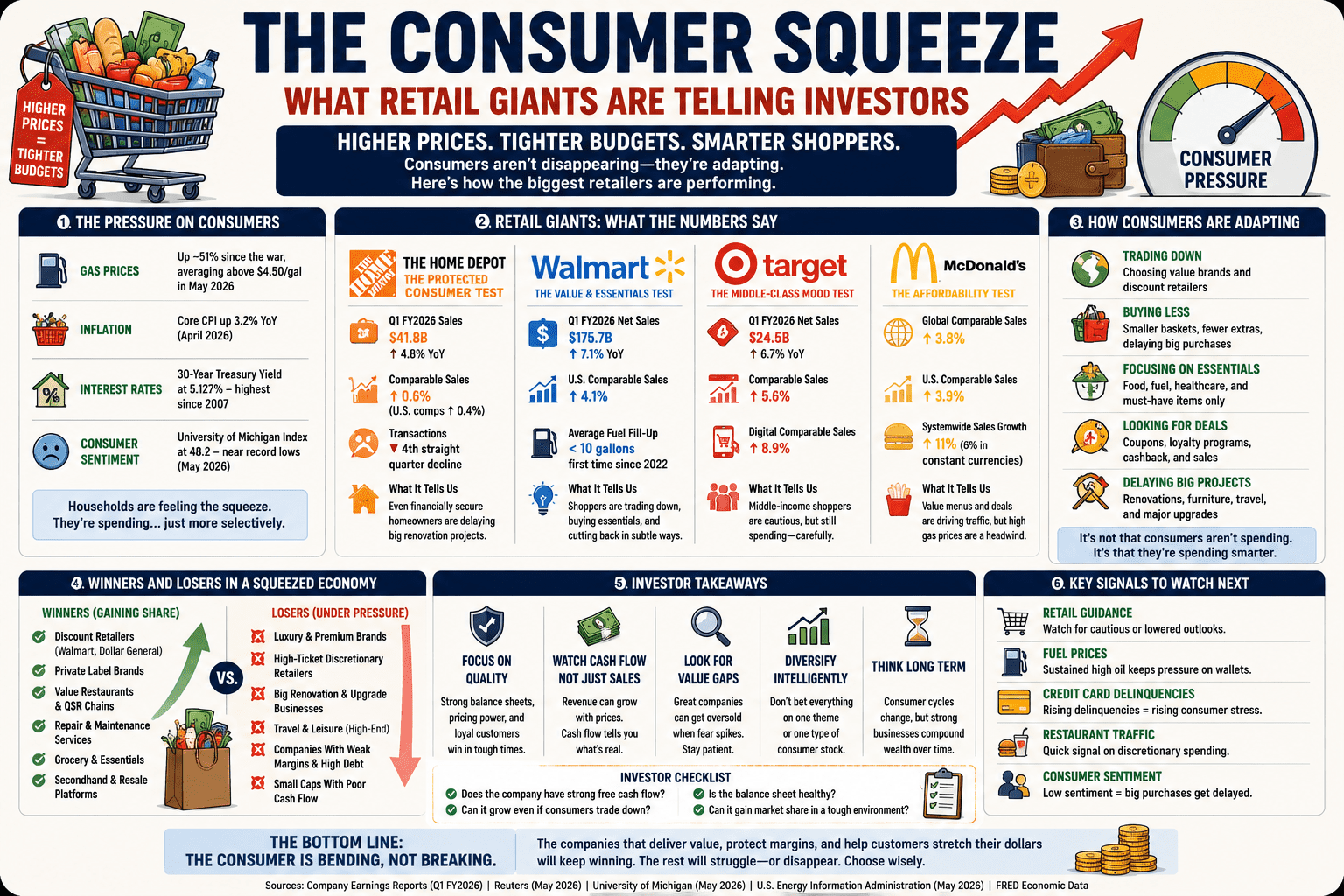

Home Depot reported first-quarter fiscal 2026 sales of $41.8 billion, up 4.8% from the prior year, while comparable sales increased only 0.6% and U.S. comparable sales increased 0.4%. Management also said underlying demand was “relatively similar” to fiscal 2025, despite greater consumer uncertainty and housing affordability pressure.

That is not a disaster report. But it is not a roaring-boom report either. The important detail is the gap between total sales growth and muted comparable sales growth. Total sales can rise because of acquisitions, new stores, pricing, or other factors, while comparable sales tell you more about demand at existing locations.

The newsletter material you provided framed Home Depot as “the ceiling” for the consumer, arguing that its shopper is one of the more protected cohorts and that if homeowners are delaying larger renovation projects, households below them may be under even more pressure. It also said Home Depot beat earnings and reaffirmed guidance, but comparable sales rose just 0.6%, while transactions had fallen for four straight quarters.

That is the investment insight: Home Depot can be a warning sign even when the headline result is not terrible. Investors should watch the mix between small repair projects and big renovation projects. If people are still fixing leaky pipes but delaying kitchen remodels, that tells you confidence is lower. They are maintaining assets, not upgrading lifestyles.

The Secret in Retail Earnings: Traffic Versus Ticket Size

One of the best investing tricks for reading retail earnings is to separate traffic from ticket size. Traffic tells you how many customers are showing up. Ticket size tells you how much they are spending per visit. The combination tells you whether a business is gaining real demand or simply charging more.

A company with rising traffic and rising ticket size is in a strong position. A company with rising traffic but shrinking basket size may be gaining shoppers who are spending carefully. A company with falling traffic but rising ticket size may be relying on price increases, not customer enthusiasm. A company with falling traffic and falling ticket size is usually in trouble.

This is why retail earnings are more useful than people think. They are not just about whether a stock beat EPS estimates by a few cents. They reveal household behavior before it becomes obvious in broader economic data.

For regular investors, this is a huge advantage. You may not have access to expensive Wall Street research, but you can still read earnings releases and ask simple questions. Are customers visiting more often? Are they buying fewer items? Is the company discounting more? Are margins holding up? Is guidance cautious?

Walmart: The Value Test

Walmart is the ultimate value test because it serves almost everyone. Lower-income shoppers rely on it for essentials. Middle-income shoppers use it to stretch budgets. Higher-income shoppers increasingly use it for convenience, delivery, and value when inflation makes even comfortable households more price-sensitive.

Reuters reported that Walmart’s first-quarter operating income rose 5% to $7.49 billion, while net sales climbed 7.1% to $175.7 billion. U.S. comparable sales rose 4.1%, U.S. e-commerce sales grew 26%, and the company kept conservative annual sales and profit targets despite solid results.

On the surface, that sounds strong. But the deeper story is more complicated. Reuters also reported that higher fuel costs reduced Walmart’s operating income by about $175 million in the quarter, and Walmart’s CFO said that if the elevated cost environment persists, the company would expect somewhat higher retail price inflation in the second quarter and second half of the year.

The most interesting detail was not just sales growth. It was the gas pump signal. Reuters reported that the average fuel fill-up at Walmart gasoline stations fell below 10 gallons for the first time since 2022, which Walmart’s CFO described as a sign of stress. That is the kind of detail common investors should train themselves to notice.

A shopper buying fewer gallons is not just a fuel story. It can be a cash-flow story. Maybe they are topping up smaller amounts because they cannot comfortably fill the tank. Maybe they are reducing trips. Maybe they are watching every dollar. That is how household stress shows up before it becomes dramatic.

Target: The Middle-Class Mood Test

Target sits in an interesting position. It is not as bargain-focused as Walmart, but it is not luxury retail either. It sells essentials, groceries, apparel, home goods, beauty products, seasonal items, and discretionary categories that reveal how confident the middle-class shopper feels.

Target’s first-quarter 2026 results were stronger than expected. Net sales grew 6.7% from the prior year, comparable traffic grew 4.4%, digital comparable sales grew 8.9%, and comparable sales grew 5.6%. Target also raised its expected 2026 net sales growth range to around 4%, two percentage points above its prior range.

That sounds encouraging, and it is. But the useful investor lesson is not simply “Target good.” It is that even in a squeezed consumer environment, companies can win if they improve execution, sharpen product mix, and give shoppers enough reason to visit.

Target’s results also show why investors need nuance. A consumer squeeze does not mean every retailer fails. It means the weak, overpriced, poorly positioned, or badly managed retailers become more vulnerable, while stronger operators can take share.

For personal finance readers, there is a lesson here too. When money is tight, households become better capital allocators. They compare prices, choose convenience carefully, and reward businesses that solve real problems. Investors should think the same way. Own companies that help customers survive pressure, not companies that depend on customers ignoring pressure.

McDonald’s: The Affordability Test

McDonald’s is one of the best affordability signals in the world. When consumers feel stressed, they may still eat out, but they often trade down. That can help fast food companies, especially those with strong brands, value menus, loyalty programs, and scale.

McDonald’s reported global comparable sales growth of 3.8% for the first quarter of 2026, with U.S. comparable sales up 3.9%. It also reported systemwide sales growth of 11%, or 6% in constant currencies, and diluted earnings per share of $2.78, up 7%.

That looks solid, but again, the details matter. Reuters reported that McDonald’s U.S. same-store sales growth missed analyst expectations, and the company saw a weak start to the second quarter as high gas prices pressured demand.

That is exactly the kind of mixed signal investors need to understand. McDonald’s can be both strong and pressured. It has scale, brand power, loyalty data, global reach, and value positioning. But if gas, rent, groceries, and debt payments squeeze customers hard enough, even relatively cheap meals become a decision.

For common investors, McDonald’s teaches a bigger principle: defensive consumer businesses are not invincible. They may hold up better than weaker brands, but they still operate in the real world. If households are stretched, traffic, mix, and pricing power can all come under pressure.

The Big Insight: People Are Trading Down, Not Vanishing

The consumer is not disappearing. That is important. People still need groceries, gas, repairs, meals, medicine, internet, phone plans, and basic household goods. The economy does not stop because people feel stressed. It changes shape.

The key phrase for investors is “trade down.” Consumers may move from restaurants to fast food, from premium grocery stores to Walmart, from big renovations to small repairs, from name brands to private labels, from new furniture to secondhand deals, and from impulse purchases to planned purchases.

This creates winners and losers. Discount retailers can gain traffic. Dollar stores may benefit, though they can also suffer if their customers get too squeezed. Private-label brands can grow. Repair and maintenance businesses can outperform big-ticket upgrade businesses. Used goods, resale platforms, and budget-focused marketplaces can gain attention.

This is where the “investing secrets” become practical. You are not trying to predict whether everyone gets rich or everyone goes broke. You are watching where the money migrates. Consumer pressure does not destroy demand equally; it redirects demand.

The Investor Playbook for a Consumer Squeeze

A consumer squeeze changes what investors should value. In easy-money environments, investors chase growth stories, flashy narratives, and long-term dreams. In squeezed environments, they become more interested in cash flow, balance sheets, pricing power, essential demand, and disciplined management.

That does not mean you should only buy boring stocks. It means boring strengths become more valuable. A company with loyal customers, low debt, strong margins, recurring demand, and steady free cash flow can survive a rough consumer cycle. A company dependent on cheap financing and impulse spending may struggle.

The best consumer-squeeze companies usually have one or more of these traits:

- They sell essentials people still need.

- They offer value when shoppers trade down.

- They have scale that lets them absorb cost pressure.

- They can protect margins without losing too much traffic.

- They generate free cash flow instead of constantly needing new capital.

- They have strong logistics, loyalty programs, or private-label strategies.

- They can gain share while weaker competitors cut back.

The trap is buying a stock just because it has fallen. A cheap-looking retailer can always get cheaper if traffic weakens, debt is high, margins collapse, or inventory piles up. A falling price is not automatically a bargain. Sometimes it is the market correctly pricing a broken business.

Small Caps and the Consumer Squeeze

Small caps deserve special attention here because they can be powerful wealth builders, but they are also more fragile during consumer stress. Many small-cap companies are more dependent on financing, less diversified, more exposed to local demand, and more vulnerable to margin pressure.

That is why “small caps” is both a great keyword and a risky investment category. When rates fall and growth expectations improve, small caps can rally hard. When rates stay high and consumers weaken, small caps can underperform because investors demand safety and liquidity.

For readers trying to maximize wealth, the secret is not to avoid small caps entirely. The secret is to be selective. Look for small caps with strong balance sheets, insider ownership, real revenue growth, positive cash flow, and exposure to durable demand. Avoid companies that are small only because they are weak.

A consumer squeeze can actually create small-cap opportunities. Local discount chains, niche service businesses, repair-focused companies, affordable food concepts, private-label suppliers, and resale platforms may benefit if they help people save money. But speculative small caps with no profits and no financing flexibility can get crushed when investors become cautious.

Personal Finance Lessons Hidden in Retail Earnings

Retail earnings are not only useful for stock picking. They are useful for personal finance. If Walmart, Target, Home Depot, and McDonald’s are all talking about value, fuel costs, cautious shoppers, and uncertain demand, regular people should listen.

The first lesson is to protect cash flow. If big companies are watching fuel, wages, margins, and inventory carefully, households should watch their own monthly expenses just as seriously. A family budget is basically a tiny income statement. Money comes in, money goes out, and the difference determines whether you build wealth or fall behind.

The second lesson is to avoid lifestyle inflation. When times feel good, people upgrade everything: cars, subscriptions, restaurants, tools, vacations, phones, furniture, and home projects. When pressure hits, those upgrades become fixed costs. The person who kept expenses lean has more flexibility.

The third lesson is to invest in productive assets. That can mean stocks, ETFs, skills, tools, a side business, a website, a resale inventory system, or anything that can improve future earning power. Consumer stress hurts less when you are building multiple paths to income.

The fourth lesson is to buy quality when others panic. This applies to investing and real life. If strong companies with durable demand get pulled down by broad market fear, long-term investors may get opportunities. But the keyword is strong. Do not confuse a temporary discount with a permanent decline.

What Readers Should Watch Next

The next signals to watch are retail guidance, credit card delinquencies, fuel prices, restaurant traffic, discount-store results, and consumer sentiment. A single quarter does not prove everything. The pattern matters more than one headline.

If Walmart keeps gaining traffic but average spend slows, that suggests shoppers are seeking value but staying cautious. If Target keeps improving traffic and sales, that suggests the middle-class consumer may be more resilient than feared. If Home Depot continues to show weak large-project demand, that suggests housing affordability and rates are still hurting confidence. If McDonald’s value strategy works, that suggests consumers are trading down rather than disappearing.

Investors should also watch margins. Sales growth gets attention, but margins reveal the cost of keeping customers. A retailer can grow revenue while sacrificing profit if it has to discount heavily, absorb fuel costs, or raise wages to keep service quality high.

This is why guidance often matters more than past results. The market does not pay for what already happened. It pays for what investors think will happen next. If management teams sound cautious, the stock can fall even after a decent quarter.

The Skeptical View: Maybe the Consumer Is Fine

There is a reasonable counterargument. The consumer may be pressured, but not broken. Walmart is still growing. Target beat expectations. McDonald’s is still producing global sales growth. Home Depot still generated more than $40 billion in quarterly sales. These are not numbers from an economy that has completely fallen apart.

That matters because fear can go too far. Investors sometimes overreact to consumer weakness and sell high-quality companies at attractive prices. If gas prices fall, inflation cools, wages hold up, and rates stabilize, consumer stocks could recover quickly.

The consumer is also adaptive. People change habits, but they do not stop living. They find cheaper stores, use loyalty programs, cook more, repair instead of replace, shop sales, and delay purchases until they feel comfortable. That adaptability can keep the economy moving longer than pessimists expect.

The correct view is balanced. The consumer is not collapsing, but the consumer is more selective. That means investors should not panic, but they should become more disciplined.

Final Verdict: The Consumer Is Bending, Not Breaking

The best way to describe the current consumer picture is this: bending, not breaking. Households are still spending, but they are making sharper choices. They want value, convenience, essentials, and proof that a purchase is worth it.

For investors, this is a useful environment if you stay patient. The market may punish weak retailers, overvalued discretionary stocks, fragile small caps, and companies with poor margins. But it may reward businesses that provide value, protect cash flow, gain share, and keep customers loyal when money feels tight.

For regular people worried about finances, the same lesson applies. Protect your cash flow. Cut waste. Build skills. Create side income. Invest gradually. Avoid panic. Look for value. Do not let a scary economy push you into desperate decisions.

The consumer squeeze is not just bad news. It is a signal. It tells you where pressure is building, where money is moving, and where smart investors should look next. If you learn to read that signal, you can make better decisions with your portfolio, your budget, and your future.

Relevant External Link

Home Depot’s Q1 fiscal 2026 results are useful for understanding the homeowner and renovation side of the consumer economy.

I feel like the economy has been bending but not breaking the last 5 years lol