Own a House, Own a Business, Own Shares: The Three Pillars of Building Wealth

Most people are taught how to earn money, but far fewer are taught how to own things that produce, preserve, or increase wealth. We learn to pursue qualifications, secure employment, negotiate a salary, and hopefully save whatever remains at the end of the month. Those are important skills, but employment income alone rarely provides complete financial security. A paycheque stops when the work stops, while a well-chosen asset may continue creating value long after it was acquired.

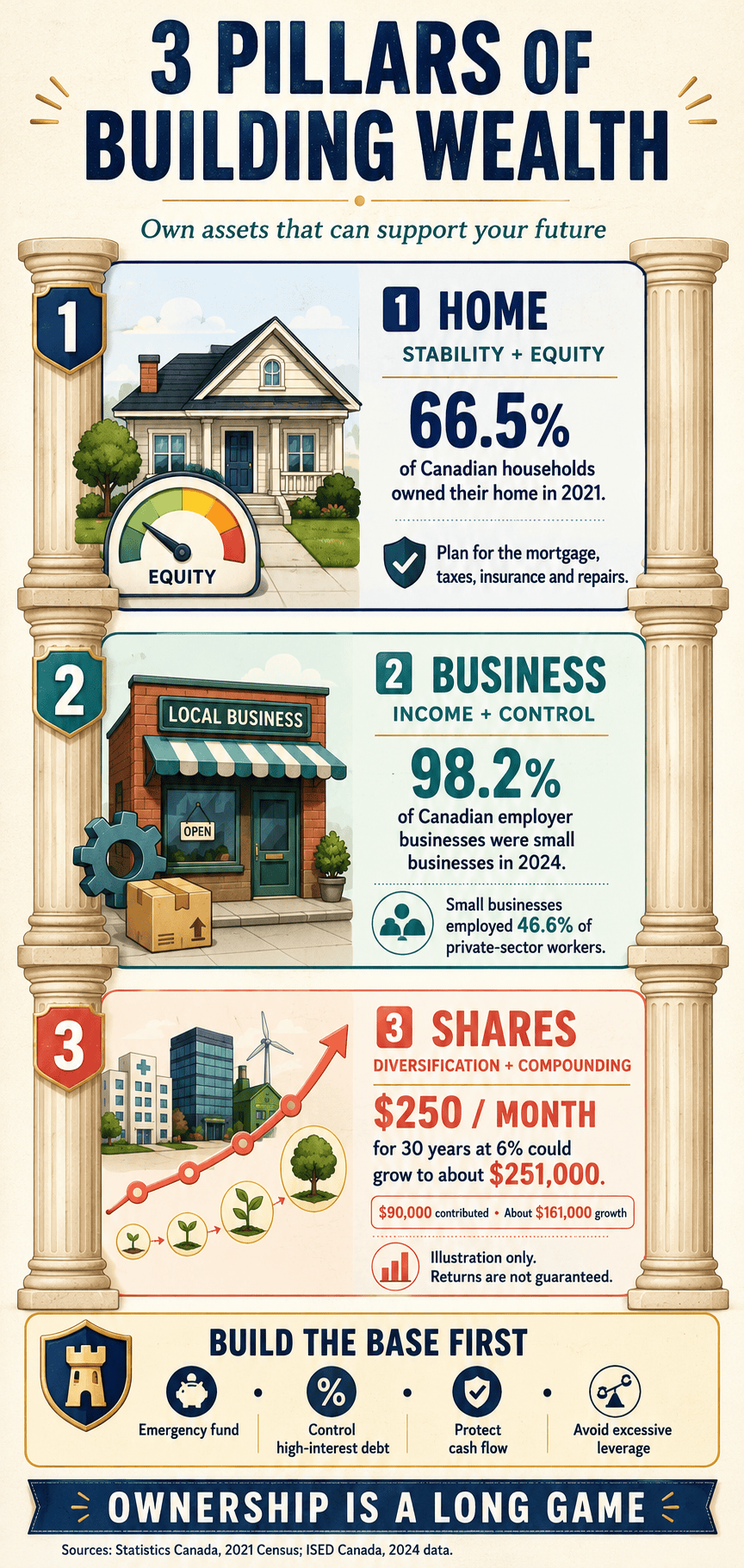

That is why the advice to “own a house, own a business, and own shares” is so compelling. Each form of ownership performs a different financial job. A home can provide stability and gradually build equity, a business can expand your earning power, and shares allow you to own pieces of productive companies without operating them yourself.

This is not a rule stating that every person must immediately purchase all three. Renting can be financially sensible, many businesses fail, and stock markets can decline sharply. The more useful interpretation is that financially secure people eventually need to own assets—not merely consume products, pay bills, and sell their time.

Quick Answer: What Are the Three Pillars?

The three pillars represent different ways of participating in the economy as an owner:

- A house can provide housing security, mortgage-free living later in life, and equity that grows as debt is repaid.

- A business can create income, professional independence, intellectual property, customer relationships, and an asset that may eventually be sold.

- Shares provide fractional ownership in publicly traded companies and access to potential dividends and long-term capital growth.

None is automatically profitable, and none is appropriate at every stage of life. The larger principle is to convert part of today’s income into assets that may strengthen tomorrow’s balance sheet.

The Difference Between Income and Ownership

Income pays for the present. Ownership helps finance the future.

An employee can earn an excellent salary and still accumulate little wealth if nearly every dollar is consumed. Conversely, a person with a moderate income can gradually build a meaningful net worth by consistently acquiring assets and avoiding unmanageable debt. Net worth is the value of everything a person owns minus everything that person owes.

Ownership changes the relationship between work and money. Instead of relying exclusively on wages, an owner may benefit from mortgage principal being repaid, business profits being retained, dividends being distributed, or investments increasing in value. None of these outcomes is guaranteed, but they provide financial possibilities that ordinary consumption does not.

This does not mean wages are unimportant. Employment income is often the fuel used to purchase a home, fund a business, and build an investment portfolio. The mistake is treating income as the final destination instead of using a portion of it to acquire productive assets.

Pillar One: Own a House

A primary residence is unusual because it is both a place to live and a major financial asset. It provides immediate utility—shelter, privacy, stability, and control over one’s living space—while potentially building equity over time. Equity is the portion of the property’s value that belongs to the owner after subtracting the outstanding mortgage and other debts secured against it.

Every mortgage payment generally contains both interest and principal. Interest is the cost of borrowing, while principal reduces the amount owed. As principal is repaid, the homeowner’s equity increases, assuming the property’s market value does not decline enough to offset that progress.

A home can also become particularly valuable later in life. Someone who enters retirement with a paid-off residence may have substantially lower monthly housing obligations than someone paying market rent. Property taxes, insurance, utilities, repairs, and maintenance remain, but eliminating a mortgage can reduce the amount of income required to maintain a household.

Why a Home Can Strengthen a Financial Foundation

Homeownership has several potential advantages:

- It replaces exposure to future rent increases with a mortgage arrangement that eventually ends.

- It encourages regular equity building through scheduled principal payments.

- It provides a physical asset that can potentially be sold, downsized, or passed to heirs.

- It allows the owner to modify and use the property, subject to local regulations and financing restrictions.

- In Canada, qualifying gains on a principal residence may receive favourable tax treatment, although the property’s use and reporting requirements matter.

A mortgage also introduces leverage. Leverage means using borrowed money to control an asset worth more than the cash initially invested. If a buyer contributes a down payment and the property rises in value, the gain is calculated on the property’s full value, not merely the down payment. However, leverage magnifies losses as well as gains, and the mortgage must still be serviced when property values fall.

A House Is Not Guaranteed to Be a Good Investment

The phrase “real estate always goes up” is dangerously simplistic. Property values can stagnate or decline, particularly in a weak local economy or after a period of speculative buying. Even when the sale price rises, transaction costs, mortgage interest, renovations, property taxes, insurance, and years of maintenance can consume much of the apparent gain.

A home is also illiquid, meaning it cannot be quickly converted to cash without a sale, refinancing, or secured borrowing. Selling may take weeks or months and usually involves legal expenses, moving costs, and real estate commissions. A person with nearly all their net worth trapped in a residence can appear wealthy on paper while struggling to cover ordinary expenses.

The Financial Consumer Agency of Canada notes that buyers should consider more than the purchase price. Closing expenses, ongoing housing costs, debt obligations, mortgage structure, and the possibility of higher payments at renewal all affect affordability. Its general guidance describes housing costs around 39% of gross household income and total debt around 44% as upper qualification measures, not spending targets. A prudent buyer often leaves a wider margin for repairs, emergencies, and changing interest rates. Financial Consumer Agency of Canada

When Renting May Be the Better Decision

Renting is not financial failure. It may be the stronger option for someone who expects to move, lacks an emergency fund, works in an unstable industry, or would need to stretch every dollar to qualify for a mortgage. Renting can also provide flexibility and shift major repair responsibilities to the landlord.

The correct comparison is not simply rent versus a mortgage payment. A realistic analysis compares rent with the total unrecoverable cost of ownership, including mortgage interest, taxes, insurance, maintenance, condominium fees where applicable, and transaction costs. The principal portion of a mortgage payment builds equity; most of the other expenses do not.

A house should therefore be purchased when it fits a person’s finances and life—not merely because homeownership appears on a wealth-building checklist.

Pillar Two: Own a Business

A business offers something employment cannot provide in the same way: ownership of the system that generates revenue. An employee is paid for contributing to someone else’s operation. A business owner controls the offer, pricing, customer relationships, processes, brand, and, within practical limits, how the profits are used.

This pillar also has the widest range of possible outcomes. A small side business may produce a few hundred dollars per month, while a scalable company may become worth considerably more than its annual profit. On the other hand, a poorly planned venture can consume savings, damage credit, and create tax or legal problems.

The point is not that entrepreneurship is an easy route to riches. It is that a functioning business can create both income and equity. Income is what the owner earns from current operations. Business equity is the value that may remain in the company’s reputation, equipment, intellectual property, systems, contracts, customer base, and ability to produce future profit.

Self-Employment Is Not Always a Business Asset

There is an important difference between owning a business and merely owning a demanding job. If all revenue depends on the owner personally performing every task, the operation may provide good income but have limited transferable value. When the owner becomes sick, takes a vacation, or stops working, revenue may stop as well.

A more durable business gradually develops assets and systems beyond the owner’s labour. These might include:

- A recognizable brand and professional website

- Documented operating procedures

- Reliable suppliers and subcontractors

- Repeat customers or contracted revenue

- A customer relationship management system

- Intellectual property, proprietary designs, or specialized methods

- Employees or contractors capable of completing routine work

- Accurate financial records that demonstrate profitability

This transformation does not need to happen immediately. Many strong businesses begin with one person selling a skill. The owner’s long-term goal, however, should be to make the operation increasingly organized, repeatable, and less dependent on one person’s memory or constant presence.

Business Ownership Does Not Require a Huge Company

The word “business” often brings to mind offices, employees, warehouses, or substantial financing. In reality, a useful business asset can begin with a narrow service, a digital product, a specialized trade, or a simple solution to a recurring problem.

A bookkeeper serving local contractors, a woodworker selling project plans, a technician maintaining small-business websites, or a tradesperson operating a well-managed service company can all build legitimate businesses. The deciding factor is not glamour or size. It is whether customers reliably pay more than it costs to deliver the product or service.

Starting small can reduce risk. A person can validate demand, establish pricing, and learn the operation while retaining employment income. This is often more responsible than quitting a job based on enthusiasm before obtaining evidence that customers will buy.

The Risks Behind the Potential

Business ownership concentrates risk. The owner may have personal savings, unpaid labour, business debt, and future income tied to the same operation. If demand disappears, several parts of the owner’s financial life can be affected simultaneously.

Legal structure also matters. A sole proprietorship is comparatively simple, but the business and owner are not separate legal persons. Incorporation may provide legal, tax, financing, or succession advantages in some situations, but it adds costs and administrative obligations and does not eliminate every form of personal liability.

Before making structural or tax decisions, an owner should consult a qualified accountant or lawyer familiar with the relevant province and industry. Good advice is much cheaper than correcting years of improper bookkeeping, missed remittances, inadequate contracts, or misunderstood liability.

Pillar Three: Own Shares

A share represents ownership in a company. When investors purchase shares, they are not merely betting on a line moving across a screen; they are acquiring equity in an operating enterprise. Depending on the company and type of share, owners may benefit from increases in market value, dividends, voting rights, or some combination of the three.

Shares make business ownership accessible to people who do not want to operate a company themselves. An investor can own pieces of banks, manufacturers, railways, retailers, technology firms, utilities, and thousands of other businesses. Unlike a private business, publicly traded shares can generally be bought or sold relatively quickly through an investment account.

This liquidity is one reason shares complement home and business ownership. A residence and private company may contain substantial value, but both can be difficult to sell. A portfolio of marketable securities provides a more divisible asset: an investor can sell a small portion without disposing of the entire portfolio.

Diversification Matters More Than Excitement

Owning shares does not mean selecting several fashionable companies and hoping one becomes the next market giant. That approach concentrates risk in individual businesses, industries, and predictions. A company can lose value because of competition, excessive debt, poor management, regulation, fraud, changing technology, or an economic downturn.

Diversification spreads capital across multiple holdings so that one failure is less likely to destroy the entire portfolio. Broad-market exchange-traded funds, commonly called ETFs, can hold shares in dozens, hundreds, or even thousands of companies. Some cover a single country or industry, while others provide exposure across multiple markets.

Diversification cannot prevent losses, especially when an entire market declines. It does, however, reduce reliance on one company or one narrow investment idea. The Ontario Securities Commission explains that investments which respond differently to economic conditions can help balance portfolio risk, although diversification has limitations and cannot guarantee returns. GetSmarterAboutMoney.ca

Compounding Rewards Time and Consistency

Shares can produce returns through dividends and capital appreciation. Dividends are distributions a company makes to shareholders, while capital appreciation occurs when an investment becomes more valuable. If earnings and dividends are reinvested, the investor may eventually earn returns on previous returns—a process known as compounding.

Compounding is powerful, but it is not smooth. Markets can fall sharply, remain disappointing for extended periods, and test an investor’s patience. Money required for an emergency, home purchase, tax payment, or other near-term obligation generally should not depend on stock-market performance at a particular moment.

That is why time horizon and risk tolerance matter. Time horizon is the period before the money will likely be needed. Risk tolerance combines a person’s financial ability and emotional willingness to withstand losses without abandoning the plan.

An Account Is Not the Same as an Investment

Canadian investors commonly use TFSAs, RRSPs, FHSAs, registered education plans, and non-registered accounts. These are account structures with different purposes and tax rules; they are not investments themselves. Cash, guaranteed investment certificates, bonds, mutual funds, ETFs, and individual shares may be held inside certain accounts when eligible.

Opening a TFSA and leaving it entirely in cash is therefore not the same as investing in shares. Likewise, buying a speculative stock inside a registered account does not make the investment safe. Investors must choose both the appropriate account and suitable investments within it.

Tax rules, contribution limits, withdrawal rules, and individual circumstances can change. Anyone making a significant contribution, withdrawal, transfer, or business-related investment decision should confirm current Canada Revenue Agency guidance or consult a qualified professional.

Why the Three Pillars Work Better Together

Each pillar has a different combination of utility, liquidity, control, and risk. The value of the framework comes from combining those strengths instead of expecting one asset to handle every financial need.

| Pillar | Primary Role | Main Advantage | Major Limitation |

|---|---|---|---|

| House | Stability and equity | Provides shelter while potentially building net worth | Expensive, illiquid, and locally concentrated |

| Business | Income and control | Offers high upside and direct influence over results | Demands work and carries concentrated risk |

| Shares | Growth and diversification | Provides liquid ownership in many companies | Volatile and outside the investor’s control |

A business owner may invest profits in diversified shares rather than leaving all wealth inside the company. A homeowner may maintain a liquid portfolio instead of directing every spare dollar toward the mortgage. An employee may own shares long before being ready to purchase property or launch a business.

This is genuine diversification across ownership types. One asset might struggle while another remains useful. A home still provides shelter during a stock-market decline, a portfolio can remain liquid when a business has a slow season, and business income may accelerate mortgage repayment or investing.

Which Pillar Should Come First?

There is no universal order. The right sequence depends on income stability, location, family needs, skills, risk tolerance, and existing obligations. Insisting that everyone purchase a home first can delay investing for years, while telling everyone to launch a business ignores the reality that not everyone wants or needs entrepreneurial risk.

For many people, a sensible sequence looks like this:

- Stabilize the foundation. Build a starter emergency fund, control high-interest debt, maintain appropriate insurance, and understand monthly cash flow.

- Begin acquiring diversified investments. Small, automatic contributions can establish the habit before income becomes substantial.

- Test a business idea cautiously. Validate customer demand and pricing before committing large amounts of capital.

- Purchase a home when the numbers and lifestyle fit. Maintain cash reserves after the down payment and closing costs.

- Strengthen all three over time. Repay debt, improve the business, and continue investing without allowing one pillar to consume every available dollar.

The order may change. A skilled tradesperson might build a profitable service business before buying shares. Someone with stable employment in an expensive city may rent and invest for many years. A family expecting to remain in one community may reasonably prioritize a home.

The Biggest Mistakes to Avoid

The three-pillar strategy becomes dangerous when ownership is pursued for status rather than financial strength. Buying the largest house a lender will approve, financing an untested business, or chasing popular stocks can create the appearance of ambition without producing durable wealth.

Common mistakes include:

- Becoming house-poor and having no reserve for repairs or income disruption

- Treating a home’s rising market value as spendable income

- Mixing business and personal finances

- Calling an unprofitable hobby a business indefinitely

- Depending on one customer for most business revenue

- Holding too much wealth in an employer’s shares

- Speculating with money needed within the next few years

- Borrowing aggressively because an asset is expected to appreciate

- Ignoring taxes, insurance, contracts, and succession planning

- Comparing progress with people who began under different circumstances

The objective is not to collect ownership titles. It is to build a resilient balance sheet.

Do You Truly Need All Three?

No. A person can become financially secure without owning a home, and entrepreneurship is not mandatory. Someone who rents affordably, earns a reliable income, and consistently invests in a diversified portfolio may build more wealth than a highly leveraged homeowner with no savings.

Similarly, a successful business owner may prefer leasing a residence for flexibility, while a homeowner with a pension may have little desire to operate a company. Personal finance should serve a person’s life, not force that life into a slogan.

Nevertheless, the three-pillar framework remains useful because it exposes the weaknesses of relying on one source of security. A paycheque can disappear, a local property market can weaken, a business can lose customers, and a stock portfolio can decline. Multiple forms of ownership create options.

A Practical Ownership Scorecard

Instead of asking whether all three boxes have been checked, evaluate whether each part of the financial system is becoming stronger:

Home

- Are total housing costs affordable without sacrificing emergency savings?

- Is the property maintained and appropriately insured?

- Is mortgage debt declining over time?

- Would the household remain stable after a temporary income interruption?

Business

- Does it generate genuine profit after all costs?

- Are business and personal finances separated?

- Are procedures, records, contracts, and taxes properly managed?

- Is revenue becoming less dependent on one customer or the owner’s constant presence?

Shares

- Are contributions consistent and tied to long-term goals?

- Is the portfolio diversified across more than a few companies?

- Do the investments match the investor’s time horizon and tolerance for losses?

- Are fees, taxes, and account rules understood?

Progress matters more than perfection. A small portfolio, modest business, and reasonably priced home can form a stronger financial base than impressive assets overwhelmed by debt and poor cash flow.

Ownership Is the Long Game

“Own a house, own a business, and own shares” should not be interpreted as a frantic shopping list. It is a reminder to gradually move from being only a worker and consumer toward becoming an owner of productive assets. The process may take decades, and each pillar should be built at a pace the household can sustain.

A home can provide stability, but it must remain affordable. A business can increase income and control, but it must solve a real customer problem and eventually produce profit. Shares can provide diversified and liquid ownership, but they require patience and the ability to tolerate market volatility.

The strongest financial plan is not the one with the most impressive assets. It is the one that continues functioning when interest rates rise, markets fall, customers disappear, or employment changes. Build ownership carefully, preserve liquidity, avoid excessive leverage, and let each pillar support the others. That is how ownership becomes lasting wealth rather than another source of financial pressure.

- Buying a Home — Financial Consumer Agency of Canada — Learn about mortgage affordability, down payments, closing costs, and the ongoing expenses of homeownership.

- Diversification — GetSmarterAboutMoney.ca — Understand how diversification can help manage investment risk and where its limitations remain.